Tag Archive for: competitive edge

EIDLs and Hazard Insurance: Your Full Guide

When running a business, there are so many things to keep track of—especially considering the COVID-19 hullabaloo we’ve experienced over the past nearly two years. Various types of insurance, Small Business Administration (SBA) loan requirements… the list goes on.

An important topic that continues to change, however, is Economic Injury Disaster Loans (EIDL) and the subsequent need for hazard insurance if it is collateralized. This brings up many questions, like

- How much does it cost?

- Why do I need it?

- How can I obtain coverage?

Each of these questions and more is answered in this article: Economic Injury Disaster Loans (EIDL) Hazard Insurance: Your Full Guide.

Let’s dive in.

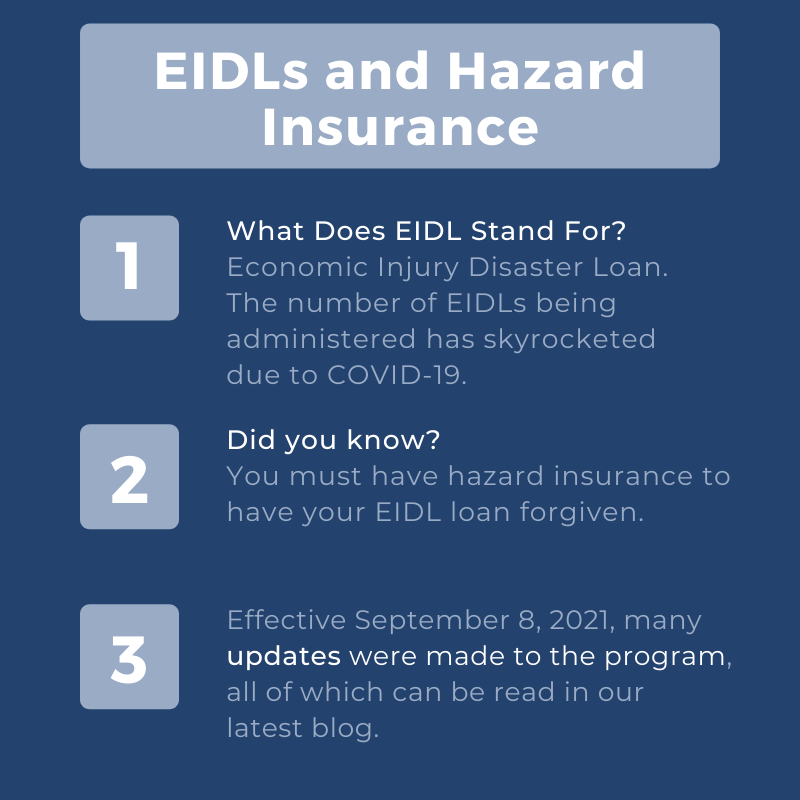

What are Economic Injury Disaster Loans (EIDLs)?

EIDLs are “the primary form of Federal assistance for the repair and rebuilding of non-farm, private sector disaster losses” administered by the SBA. “The disaster loan program is the only form of SBA assistance not limited to small businesses.”

An Update on EIDL

Over the summer, many small business owners received an alarming email from the EIDL program through the SBA.

As part of the EIDL requirements, you must have hazard insurance in order to apply for the EIDL loan. In the email from the SBA sent earlier this year, individuals were informed that those who had received the EIDL loan, must present proof of insurance in order to have their loans forgiven.

Here’s a look at what the email said.

The Email Stated:

“The SBA is launching a new round of EIDL Advances – called Targeted EIDL Advance – which provides eligible businesses with $10,000 in total grant assistance. If you received the EIDL Advance last year in an amount less than $10,000, you may be eligible to receive the difference up to the full $10,000. The combined amount of the Targeted EIDL Advance and any previously received Advance will not exceed $10,000.”

Along with Information Claiming That:

“Businesses eligible for the Targeted EIDL Advance must meet ALL the following eligibility criteria:

- Located in a low-income community, as defined in section 45D(e) of the Internal Revenue Code. The SBA will map your business address to determine if you are in a low-income community when you submit your Targeted EIDL Advance application.

- Suffered economic loss greater than 30 percent, as demonstrated by an 8-week period beginning on March 2, 2020, or later, compared to the previous year. You will be required to provide the total amount of monthly gross receipts from January 2019 to the current month-to-date.

- Must have 300 or fewer employees. Business entities normally eligible for the EIDL program are eligible, including sole proprietors, independent contractors, and private, nonprofit organizations. However, agricultural enterprises, such as farmers and ranchers, are not eligible to receive the Targeted EIDL Advance.”

The SBA said loans won’t be forgiven unless you have proof of insurance coverage. If you’re looking to check which COVID-19 loans are forgivable, visit this list.

But Why Do You Need Hazard Insurance to Qualify?

“The Small Business Administration is a lender. Just like any other lender, the SBA is trying to protect their loan’s collateral from unforeseen circumstances,” says Naomi Bishop on hazard insurance. Therefore, all borrowers must obtain hazard insurance within 12 months of loan approval. Additionally, coverage must be maintained throughout the life of the loan.

Additionally, when applying for a loan, you guarantee a loan by offering assets as collateral. For example, financial (i.e. cash and cash equivalents), physical (real estate), vehicles, and so on.

If you then default on an SBA loan, the lender has the right to seize and sell assets as repayment. Even others’ collateral may be at risk if they signed a guarantee on the loan. For this reason, insurance is crucial to keeping your business and others safe.

More on Hazard Insurance

Under the requirements for the EIDL, the SBA requires that your business has hazard insurance to cover 80% of the loan amount. Hazard insurance is a term for coverage that may be included within several different types of property coverage.

If you have any kind of business property insurance, you are likely covered. In fact, commercial property insurance is considered hazard insurance. This coverage protects your company’s physical assets, like buildings, furniture and equipment, supplies, computers, inventory, customer’s goods, signs, fencing, and even lost income from damage or loss.

The SBA does not allow personal hazard insurance to be considered for loans. Business auto insurance is also not allowable coverage for this requirement.

What is Happening Now?

Effective September 8, 2021, many updates were made to the COVID EIDL program. All of which can be read in full here on the SBA website.

The impact of the primary policy changes include:

- Higher loan amounts are available

- Increase[d] use of funds flexibility

- SBA automatically defers for 24 months from loan origination

- Simplifies affiliation rules for all industries…

- Created additional way[s] to meet program size standards… to include industries uniquely impacted by COVID-19 [that] continue to experience significant economic hardship

- Introduces maximum cap on corporate groups

Do You Have the Right Coverage and Correct Amounts to Satisfy Your SBA Loan?

As previously mentioned, the SBA requires that at least 80% of your loan amount is covered with hazard insurance. It may be beneficial to have 100% of your business property value covered with hazard insurance. If you received EIDL funds without coverage, you should contact your insurance agent as soon as possible.

There are a few other rules related to the insurance coverage that the SBA has stated:

- The insurance must be in the name of the business and must show proof of business property.

- If someone is a sole proprietor, and they have a DBA (Doing Business As), the DBA must be on the policy.

How Much Does Hazard Insurance Cost?

The premiums that one pays for hazard insurance is dependant on several factors, including:

- Selected limits and deductibles

- Type of coverage

- Where you live (some states are more prone to natural disasters than others)

Although this is not an end-all-be-all formula, for homeowners, the annual cost of hazard insurance typically costs between 0.25% to 0.33% multiplied by the purchase price of your home.

Hazard insurance doesn’t have to cost an arm and a leg. By comparing rates with the help of Competitive Edge Insurance, you’re sure to get the best deal for your business while making sure you stay compliant with the SBA’s requirements.

Curious about the difference between hazard insurance and high-risk insurance? Competitive Edge specializes in high-risk insurance— learn “What Classifies High Risk.”

How does Workers’ Compensation Insurance Work?

Picture this scenario: You’re at a construction site and a worker falls off the roof and falls and breaks their leg onto floor tiles, also breaking the tiles. What would be covered in that situation, the leg or the tiles?

What is Workers’ Compensation Insurance?

Workers’ compensation insurance are policies that provide medical benefits and wage compensation to workers injured on the job, in exchange for eliminating their right to file a lawsuit against their employer’s negligence.

Workers’ compensation benefits are designed to help employees if they are unable to work, cover medical expenses, as well as other expenses and rehabilitation costs associated with disability or illness. As you look to explore workers’ compensation options, it’s important to look for one that provides adequate coverage and compensation for your employees.

When you invest in a properly designed policy, it ensures you and your employees remain financially secure. It’s also important to look at the specific benefits that are offered within your policy. Typical workers’ compensation insurance policies cover medical benefits.

So, the worker’s comp covers the worker’s injury for falling off the roof.

What is Covered with Workers’ Compensation Insurance?

Specific workers’ compensation laws vary depending on your state; however, the most common compensation states that require workplace injury insurance include the following:

- Payment for lost wages

- Vocational rehabilitation

- Permanent disability

- Temporary disability

- Medical costs and treatment

Bonds

One helpful way to understand this scenario is knowing the difference between performance and payment bonds.

Payment Bonds

In simple terms, a payment bond enforces that everything must be paid once a project is completed. Payment bonds are also surety bonds and are required for most state projects based on the Miller Act.

The Miller Act was passed by the U.S. General Services Administration Public Buildings Service (GSA) with the intention to explain how payment bonds protect subcontractors and suppliers.

The GSA responds to any reports of nonpayment, following the legal action needed and protected by the Miller Act. The GSA states that “the Miller Act requires that prime contractors for the construction, alteration, or repair of Federal buildings furnish a payment bond for contracts in excess of $100,000.”

Payment bonds additionally play a major role in construction. As an insurance company, we have relationships with carriers who understand the specifics of construction risk and can provide better solutions, better prices, and more comprehensive coverage—even for hard-to-place and high-risk companies.

Performance Bonds

The main differentiator between payment and performance bonds is that a performance bond ensures the employer is satisfied with the job. While both are surety bonds, performance bonds can be helpful in industries apart from construction.

A performance bond, according to Investopedia, “ensures the completion of a project. Setting these two together provides the proper incentives for laborers to provide a quality finish for the client.”

Any type of bonding will cover e tiles or building materials that were broken.

Overview

If an employee falls off the roof and hurts their leg and breaks the tile, the Workers comp covers the worker’s injury for falling off the roof. Bonding covers the broken tiles from his attempt not to fall off the roof.

The first step is to show us under the hood so we can help you find the right carrier and coverage to protect your business today and always.

Read about Worker’s Compensation for Independent Contractors here.

World Polio Day

Competitive Edge’s very own CEO, Brenda Jo Robyn has a passion for charitable giving. Because of Brenda Jo’s previous career as an Epidemiologist who specialized in immunizations, she places special attention on Polio research. As October 24 is World Polio Day, we wanted to get Brenda Jo’s insight into what World Polio Day really means to her.

What World Polio Day Means to Brenda Jo:

“I belong to the rotary club of Coronado and one of the things that I specifically work on is a fundraiser called End Polio Now, which raises funds to immunize children across the globe.

Over the last few years, we have raised $2.1 billion to protect over 3 billion children and 122 countries from Wild Polio Viruses, two have been eradicated, and one is still active. And the only countries in which Polio exists in the wild are Pakistan and Afghanistan. This year, we only had two reported cases in January. However, between 2018 and 2020, there hasn’t been as much access to services for families and children. And in those two countries in 2020, there was a three-month break from providing immunizations due to COVID-19.

They couldn’t go around and go from town to town and, and tried to tribe. Due to recent events, it has become increasingly challenging in Afghanistan and the immunization locations have been closed down. There’s a big concern right now on how this will play out and affect the future.

Currently, there’s an estimate of 3 million children that remain, un-immunized. And why is this a concern? Well, it can lead to an outbreak. Refugees are being accepted in countries all over the world, and we don’t know who is immunized and who is not immunized as they come. We really have to focus on those children as they’re coming in and treat them all as if they are not immunized.”

Understanding World Polio Day

World Polio Day is an effort to draw attention to the End Polio Now organization working to eradicate the wild poliovirus in both Afghanistan and Pakistan, as well as increase immunizations in countries that are at greater risk, like Africa.

In order to eradicate the wild poliovirus, high-quality immunization campaigns must be carried out to polio-affected and high-risk countries. Rotary has played a huge role in contributing to Polio eradication.

What is Rotary?

Brenda Jo is a part of the Rotary Club, which provides her with various opportunities to connect and give back to the community at large.

“Rotary is a global network of 1.2 million neighbors, friends, leaders, and problem-solvers who see a world where people unite and take action to create lasting change–– across the globe, in our communities, and in ourselves.”The main goal of Rotary is to serve others in the form of charitable works, giving, and time. Brenda Jo loves being a part of Rotary as it gives her the opportunity to make a real difference in the world. If she can impact just one life in a positive way, it is all worth it.

What Factors Reduce My Commercial Insurance Premiums?

Do you know the in’s and out’s of commercial insurance? Test your premium knowledge by taking the quiz below!

Need some more help after taking that quiz? Read more about the four types of insurance you should have for your business here!

Hiring in California: How to Reduce Your Risk

Hiring new employers can be risky for company culture and the bottom line.

Since new employees are hard to come by, sometimes the decision to hire is rushed and there can be increased risks involved with the hiring process.

Even Brenda Jo Robyn, founder of Competitive Edge Insurance, screens employees pre-hire on Motor Vehicle Records (MVRs). This checks if they have a clean record and can they legally drive for your company, which ultimately will help with company rates.

Screening Employees

Who you work with matters.

On one hand, creating a positive company culture will benefit your employees and overall employee retention, which reduces financial and social risk. One way to create this company culture concerns how you screen potential employees in order to avoid a toxic environment.

A DMV screen costs 60 dollars and has proved to be worth the extra step. This DMV screen includes a general background check and driver’s license check.

It’s important to require DMV screens every year. This can save your company a lot of time and money in the long run by retaining the right employees.

Lastly, if your employee is driving on company time, it is important to make sure that the employee has their own car insurance.

Intellectual Property

In California, your client list can be considered intellectual property. In each employee offer letter, however, it’s crucial to have a separate section outlining that all clients will stay connected with the company if they were to leave.

If you have failed to do so already, you might consider reaching out to current employees and stating the new company policy.

Physical Space

The separation of class (for example, warehouse space vs. office space) for employees might take a couple of extra steps as a business owner but will reduce risk when hiring new employees. The separation between the physical warehouse and office space is the main separation to be considered as a business owner.

There are regulations for how the space is separated. For example, for some, areas being separated by chain link is considered acceptable.

Invest in EPLI

The Employer’s Professional Liability, also known as EPLI, causes different claims to arise from employees. There are a few ways to protect your business from a flood of EPLI claims. Employee lawsuits are rising and in return, settlements are becoming even more expensive. Although there are different types of insurance, workers’ compensation and EPLI are both ways to reduce risk with employee benefit plans.

EPLI is crucial to invest in as a company if it comes to a disgruntled employee—even if you are a small business. In the chance that your company gets sued, your EPLI insurance will cover it.

High-Risk Coverage

High-risk insurance addresses companies whose coverage was either terminated because of a claim, those who are new and cannot get coverage because of industry risk, or those who have experienced drops in revenue or industry disruption such that carriers are broadly refusing coverage.

You might be wondering, what risk class am I in? Luckily, there are various ways to determine this subgroup:

“An insurance risk class is a way for insurers to underwrite policies based on one’s belonging to a particular risk group.

People in each risk group will generally share similar characteristics that help insurers better estimate the chances that the policyholder will file a claim

Riskier risk groups will pay higher premiums—for example, people who are sick, older, or have a poor driving record.”

As a business owner, it is important to put the gates, systems, and processes in place to protect yourself, and Competitive Edge is here to help!

We follow the practices we write about because we believe in the importance of preventative risk. For those who are interested in reading more about what classifies as high risk, read on.

Bundling Insurance: Pros and Cons

If you’ve ever seen a Geico or Progressive commercial, you have probably heard the term “bundling insurance” thrown around, but is it actually worth it as a commercial provider?

Bundling insurance is when you choose to get multiple faucets of insurance through the same company. While it can sometimes save you money, there are potential downfalls as well.

Pros of Bundling Insurance

For commercial insurance, the pros of bundling your insurance might include:

Higher Savings

There are multi-policy discounts that might be applied to your bundled insurance. Depending on the provider and your personal preference, the discount can range anywhere from 5 to 25%.

Less Clutter

Mehmet Murat Ildan said, “If you have a complex life, make it simple; if you have a simple life, continue it that way!”

If you’re a small business owner, the concept of a simple life might be long gone—the pursuit of your passion can take up all the hours in the day. This is why finding small ways to declutter your life is crucial to finding balance.

Bundling your insurance might be a small way to organize your life and finances.

Insurance Security

If you make any claims on one type of insurance but are covered by the same company for another type, you are less likely to be dropped by them.

Cons of Bundling Insurance

Not Always Cheaper

While one of the main draws towards bundling insurance is saving money, there are cases where this isn’t the case. However, this all depends on your history. If you have a poor credit score or traffic violations, this might hinder your chances of getting a higher discount for bundling (likely in the 5% range compared to 20%).

You’re Stuck

If you choose to bundle your insurance through the same company, there isn’t a ton of room to look for other rates. If you’re bundling your insurance through the same company, they might raise your rates without much room for discussion.

Keep in Mind

If you do feel like bundling your insurance, there are some guidelines you can follow to ensure you understand what you’re getting into (even though there are short and long-term benefits of bundling).

- Evaluate all third-party options

- Compare quotes

- Keep an open mind

Contact us at Competitive Edge today for information on bundling insurance!

Four Types of Insurance Coverage for your Business

There are so many options for insurance that it can be overwhelming to know which research steps to take as a business. At Competitive Edge, we help you navigate what coverage best fits you and your business.

Health and Wellness

Niche beauty insurance solutions can miss areas of business insurance that might bridge gaps in the event of falls or other general liability claims. With health and wellness insurance, unique situations are bound to arise depending on your business’s current environment and changes.

The various Health and Wellness sectors that Competitive Edge caters to include:

- Beauty

- Spa Owners

- Hair Salon Owners

- Nail Salon Owners

- Fitness

- Yoga Studio Owners

- Pilates Studio Owners

- Dance, BarreFit, and Additional Exercise Studio Owners

- Martial Arts Studio Owners

- Health

- Naturopathy Practices

- Audiologists

- Speech and Occupational Therapy Centers

- Alternative Therapy Centers

- Acupuncturists

To provide you with the right coverage from the right carrier, we need to know about your business. It’s not enough to put all cosmetology companies in one box, all spas in another, and all beauty product companies in yet another pre-planned box.

Cyber Liability

Cyber liability is a growing industry because of the evident rise in technology, and the hacking that comes with progress.

Does this sound like news to you? Don’t worry—we already wrote an article here for you to read about reducing cybersecurity risk.

It’s important to understand what might be covered under your cyber insurance policy.

- Data Breaches

- Intellectual Property Rights

- System Failure

- Damages to a Third-Party System

- Cyber Extortion

- Business Interruption

Traditional business liability insurance likely won’t cover any cyver risks associated with your business.

Bonding

Surety bonds offer an important secondary level of coverage.

A surety bond is a contract involving three parties. It is a promise to be liable for the debt, default, or failure of another. These three parties include:

- The Principal: The party that purchases the bond and undertakes the obligation to perform the act as promised.

- The Surety: An insurance company that guarantees the obligation to be performed. If the principal fails to perform the act as promised, the surety has a contractual obligation for the losses.

- The Obligee: The party who requires and receives the benefit of the surety bond.

There are two categories of surety bonds: contract surety bonds and commercial surety bonds.

Contract surety bonds are typically written for construction projects. If a contractor defaults, the surety company is obligated to find another contractor to complete the contract. Another option for the surety company is to compensate the project owner for the financial loss incurred. There are a few bond types of contract surety bonds.

Contract sureties are required during a federal construction contract valued at $150,000 or more. State and municipal governments have similar regulations. Note that contract sureties may also be used with a private owner.

Commercial surety bonds, on the other hand, cover a broader range of surety bonds. These are required of individuals and businesses by federal, state, and local governments.

These bonds can be required by the government to obtain a license. For example, mortgage brokers, contractors, and auto dealers may be required to obtain a license or permit bond. These bonds can also be required to protect various statutes, regulations, ordinances, and other government entities.

General Business Insurance

General business insurance covers areas such as property damage, bodily injury, product liability, libel, slander, and copyright infringement.

Hindsight is no place for general business insurance conversations as lawsuits are a sad reality for many businesses. Just one bodily injury or property damage claim can take away everything you’ve worked so hard to build. General liability insurance provides businesses with coverage for most damages, injuries, medical costs, legal fees, and settlements in the case that you’re being sued.

Construction Insurance

Shock losses from large claims can make it difficult to get affordable insurance in the high-risk field of construction. If your insurance was canceled or non-renewed, we can help.

Our depth of experience and exemplary reputation with the carriers we work with can find a home for your hard-to-place and high-risk clients can find the right coverage. The fact is, every business can find coverage, you just have to take the time and know where to look.

The businesses we work with include:

- Roofing

- Construction

- Commercial Property

- Commercial Real Estate

- General Liability (CGL)

Errors and Omissions Insurance

In the CRE industry, agents are at higher risk of being accused of failing to meet a client’s expectations, failing to document decisions or actions, or failing to act in a customer’s best interest. This could be an error on a title or an oversight in a property listing, which could lead to a costly lawsuit.

Errors and Omissions (E&O) insurance covers against financial losses from lawsuits filed as a result of an agent’s work in the real estate profession. These policies cover liability related to the following issues:

The client may claim that you made an error that led to financial loss. In a lawsuit regarding professional mistakes, you may be at risk of losing big, considering the size of commercial property transactions.

An example of this is when a real estate agent misstates the square footage of a property. If the agent has Errors and Omissions Insurance, however, they may be covered for attorney’s fees, court costs, settlements, judgments, and fines.

Potential E&O Exclusions

While it’s important to know what E&O insurance covers, it’s also important to understand potential exclusions. Some common exclusions in E&O coverage include claims resulting from dishonest or criminal acts. As well as claims associated with a polluted property. If any agent causes bodily harm or death to another person, or the agent causes damage to someone’s property, their claims will not be covered under E&O insurance.

In the CRE industry, it’s more common to face a lawsuit related to errors and omissions so it’s best to be covered before you need it. Roger J. Stewart is an expert in providing coverage for real estate professionals and has helped various CRE investors and agents avoid risk and save money throughout the years.

At Competitive Edge Insurance, we work with insurance carriers across the country to place all types of business coverage. We are always seeking out new insurance companies to write hard-to-place and high-risk business insurance.

Don’t let cancellation dissuade you from finding comprehensive coverage, we can help!

Contact us today at Competitive Edge to find out more information.

What Classifies High Risk?

At Competitive Edge, we specialize in high-risk insurance. We often get the question, “What is high-risk insurance, and how do I know if I need it?”

Well, the answer is, if you’re a small business owner, general contractor, or even car owner, you likely need high-risk insurance. Depending on the industry you’re in, however, it can be difficult to fund coverage or losses.

There are a couple of ways to identify what classifies high-risk insurance.

Risk Class

Investopedia defines risk class as, “A group of individuals or companies that have similar characteristics, which are used to determine the risk associated with underwriting a new policy and the premium that should be charged for coverage.”

There are some main points that are needed to understand the risk that is associated with coverage:

- “An insurance risk class is a way for insurers to underwrite policies based on one’s belonging to a particular risk group.

- People in each risk group will generally share similar characteristics that help insurers better estimate the chances that the policyholder will file a claim

- Riskier risk groups will pay higher premiums—for example, people who are sick, older, or have a poor driving record.”

Once you determine if you qualify for high-risk insurance, there are additional factors that will determine your premium. These might include:

- Age

- Amount of coverage

- Number of years the coverage is guaranteed

- Risk class

- And more!

Additional Classifications

One example of a scenario of hard-to-place insurance is from our very own founder, Brenda Jo Robyn of Competitive Edge Insurance. Brenda Jo had to pay an extra $15,000 in order to get her directors on board for her project.

If you have had excessive losses, shock loss, or are a startup (tech and service), it can be challenging to get professional liability coverage. There are, in fact, some extreme costs associated with high-risk coverage.

So, even the professionals have dealt with the difficulties and hoops that surround high-risk insurance (trust us, we get how frustrating it can be to navigate). That’s also why we’re here to help!

Contact Us Today!

Competitive Edge Insurance can help you perform a comprehensive review of all your risk exposure.

Reach out today for more information from our experts on high-risk insurance!

BEWARE: Workers’ Comp Insurance for Independent Contractors

As you may know, most states require employers to have workers’ compensation insurance. These insurance policies can help recover most of your employee’s lost wages while they recover from a work-related injury or illness.

It also helps to cover your employee’s medical expenses as it provides their family with death benefits if they, unfortunately, pass away.

What is Workers’ Compensation Insurance?

Workers’ compensation insurance are policies that provide medical benefits and wage compensation to workers injured on the job, in exchange for eliminating their right to file a lawsuit against their employer’s negligence.

Workers’ compensation benefits are designed to help employees if they are unable to work, cover medical expenses, as well as other expenses and rehabilitation costs associated with disability or illness. As you look to explore workers’ compensation options, it’s important to look for one that provides adequate coverage and compensation for your employees.

When you invest in a properly designed policy, it ensures you and your employees remain financially secure. It’s also important to look at the specific benefits that are offered within your policy. Typical workers’ compensation insurance policies cover medical benefits.

What is Covered with Workers’ Compensation Insurance?

Specific workers’ compensation laws vary depending on your state; however, the most common compensation states that require workplace injury insurance include the following:

- Payment for lost wages

- Vocational rehabilitation

- Permanent disability

- Temporary disability

- Medical costs and treatment

How to Prepare for Employee Claims

Accidents happen. It’s part of life. It doesn’t matter how safe your business is, there’s always the chance an employee will get sick or injured on the job. For this reason, nearly every state requires business owners to have coverage for their employees. Different states, however, have various regulations.

Ensure you have an expert on your team to help understand what your specific business needs are. For example, if your business is in California, you are required to obtain workers’ compensation insurance even if your business is as small as just one employee. In Florida, however, you need this coverage if you have at least four employees.

Signing up for workers’ compensation depends on the location of your business. Typically, states recommend you purchase workers’ compensation insurance through a private insurance company, while others may require you to buy it through a state-run insurance fund.

It’s also important to understand the cost associated with investing in workers’ compensation insurance. The risk associated with your specific business will determine the cost of your insurance payments. This all sounds pricey, but remember: the costs associated with not having workers’ compensation insurance might be the motivation you need to start considering your options.

Without workers’ compensation insurance, you put yourself and your business at risk of fines, and could even face potential jail time for not complying with regulations. If an employee runs into a problem that would have been covered by workers’ compensation insurance, you may be responsible for covering their expenses, and you may also open yourself up to litigation.

What You Need to Know About Workers’ Compensation as an Independent Contractor

Every contractor needs general liability insurance. While the law does not require it, it is considered best practice to ensure against the kinds of injuries and lawsuits general liability is targeted to.

Large contractors may own commercial buildings that require property insurance, where smaller contractors or those with a specialty may need different coverage.

At Competitive Edge, we don’t claim to know your needs until we talk to you. What’s right for one company may not be a choice that meets your needs. Even if you have suffered a shock loss, large claim, or lawsuit, and find that your options have narrowed, we can work with you.

The first step is to show us under the hood so we can help you find the right carrier and coverage to protect your business today and always. Contact Competitive Edge Insurance today for more information about high-risk coverage today!